Short Analysis: AutoStore (AUTO:OL)

Momentum in the Grid: The Turnaround Thesis for AutoStore Holdings.

Quick View

Ticker: OSE: AUTO

Price: 12.5 NOK

Market Cap: ~42.9 Billion NOK

Rating: Attractive (Speculative)

Category: Turnaround / Fast Grower (Re-emerging)

TBFG Verdict: A high-moat technological leader showing a clear V-shaped recovery in order intake, where binary buyout optionality and a massive institutional “anchor” at 17 NOK create a compelling risk/reward profile for the bold investor.

TBFG Bottom Line

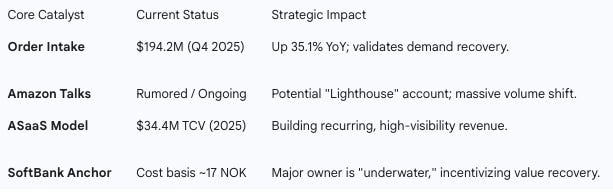

AutoStore has completed its “valley of death” phase. While our previous analysis focused on the 2024–2025 revenue contraction, the most recent quarterly data reveals a powerful shift in momentum: Q4 2025 order intake surged 35.1% year-over-year to $194.2 million, signaling that the “wait-and-see” period for capital expenditure is ending. For the risk-tolerant investor, the current 12.5 NOK price offers an entry point well below SoftBank’s average cost of 17 NOK, providing a psychological and strategic “floor.”

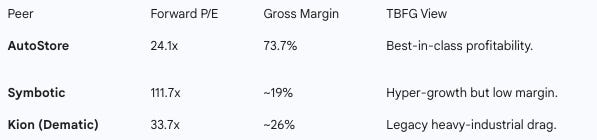

The potential for a transformational deal with Amazon or an outright buyout represents a high-alpha catalyst that is not yet priced into a 24.1x forward multiple. We are shifting from a skeptical “Overpriced” to a “Speculative Buy,” as the fundamental quality of the 70%+ gross margin remains intact while the growth trajectory is finally re-aligning with the technological moat.

Business Snapshot

AutoStore is the global standard-setter for “Cube Storage Automation.” Its proprietary aluminum grid and robotic retrieval system provide the highest storage density in the warehouse automation market, allowing customers to store 4x more inventory in the same footprint. The company operates a high-margin, capital-light “partner-led” model, selling through 23 global integrators like Swisslog and Dematic, who handle the low-margin installation and maintenance.

Management & Governance

Under CEO Mats Hovland Vikse, AutoStore has shifted from “growth at any cost” to “operational discipline.” This was evidenced by the decisive termination of the underperforming B1 Robot line in 2025, which, while incurring a $8.5 million write-down, focused R&D on the higher-throughput R5 Pro and software optimizations.

The governance structure is heavily influenced by SoftBank and THL Partners. SoftBank’s average entry price of approximately 17 NOK is a critical data point for the risk-investor. In a “The Boring Finance Guy” framework, we look for alignment; SoftBank is currently sitting on a ~26% unrealized loss at the 12.5 NOK level. This suggests that the board will be aggressively pursuing catalysts—such as the rumored Amazon partnership or a strategic sale—to realize value above that 17 NOK watermark.

Market & Competitive Landscape

AutoStore’s moat is built on 3,200+ patents and an 18-month average payback period for its customers. The 2023 settlement with Ocado effectively removed the only existential legal threat to its “cube” architecture, granting AutoStore hardware exclusivity for the foreseeable future.

While Autonomous Mobile Robots (AMRs) from Hai Robotics and Locus Robotics are faster to deploy, they cannot match AutoStore’s density. The launch of CarouselAI in 2025—AutoStore’s first AI-driven piece-picking solution—directly counters the AMR threat by integrating end-to-end fulfillment into the grid, making the “human-less warehouse” a commercial reality.

Financial Trajectory: The Turnaround Signal

The “Risk-Investment” thesis rests on the Q3 and Q4 2025 results, which broke the trend of declining performance.

Revenue Rebound: Q4 2025 revenue hit $179.7 million, up 29.3% sequentially from Q3.

Margin Integrity: Despite the 2025 market volatility, gross margins climbed to 73.7% in Q4, proving the company’s immense pricing power remains unbroken.

Debt De-risking: Management refinanced $500 million in debt in late 2025, extending maturities and providing $350 million in revolving liquidity.

Owner Earnings

We calculate Owner Earnings to strip away the “accounting noise” of the 2019 acquisition.

Owner Earnings = (Net Income + Depreciation + Amortization) - Total CapEx

Using 2025 Full Year Data:

Net Income: $81.8 million.

Depreciation: $18.7 million.

Amortization (mainly PPA): $42.2 million.

Total CapEx (PP&E + Intangibles): $48.2 million.

Calculated Owner Earnings (2025): $81.8 + 18.7 + 42.2 - 48.2 = $94.5 million.

At a $3.7 Billion market cap, this is a 2.5% Owner Earnings Yield.

While low for a “Boring” company, it is a significant improvement from the Q1 2025 “air pocket” and reflects a business that is now self-funding its R&D and expansion without diluting shareholders.

Growth Drivers & Strategic Optionality

Talks with Amazon represent a binary outcome. If AutoStore becomes a tier-1 supplier for Amazon’s micro-fulfillment strategy, the 2026–2027 revenue estimates will be revised upward by 20-30%. Even more significant is the “Buyout” risk: With Amazon’s history of acquiring its core automation providers (e.g., Kiva Systems), AutoStore at a 24x forward multiple is a cheap acquisition for a $2 trillion giant looking to own the world’s most efficient storage IP.

The shift to a subscription model (AutoStore-as-a-Service) signed $34.4 million in total contract value in 2025. This transforms the company from a cyclical equipment seller into a predictable software-and-service provider, which typically earns a 5-10x higher P/E multiple over time.

Financial Quality, Cyclicality & Execution Risk

In a Pre-Mortem analysis, why would this risk-investment fail?

Tariff Fragility: The 25% U.S. tariff on metals and automation equipment is the primary threat. If AutoStore cannot successfully shift assembly to a domestic U.S. partner, their 18-month payback period could extend to 24+ months, cooling demand in their largest growth market.

Technological Shift: If the market moves permanently toward “flexible” AMRs that don’t require floor-bolted grids, AutoStore’s $1 billion in “Cube” goodwill could become a stranded asset.

Buyout Failure: The current momentum is partially fueled by M&A rumors. If a deal with Amazon falls through and growth stalls at a “steady” 10%, the stock could re-rate to 15x earnings, implying a drop back to the 7-10 NOK range.

Valuation

PEGY Ratio

PEGY = P/E / (Growth Rate + Dividend Yield)

P/E (Forward): 24.1.

Historical Growth (2017-2023): 42%.

Projected Growth (Turnaround Case): 25% (assuming Amazon deal or market recovery).

Dividend Yield: 0%.

PEGY = 24.1 / (25 + 0) = 0.96

A PEGY below 1.0 is Peter Lynch’s classic signal for an undervalued growth stock. At 12.5 NOK, the market is pricing in “Base Case” survival, not “Bull Case” re-acceleration.

TBFG Positioning View

Verdict: ATTRACTIVE (Speculative).

AutoStore is no longer a falling knife. The Q4 2025 results confirm that the “floor” is in. The stock is a rare combination of a high-margin cash generator and a high-alpha speculative play.

Buy Zone: 10 - 13 NOK.

Target Price: 17 NOK (SoftBank parity) to 22 NOK (Strategic premium).

Position Sizing: 5% of portfolio. The binary nature of the Amazon/Buyout catalyst warrants a larger-than-normal “risk” allocation, but the tariff risk prevents it from being a “Core” position.

Trigger to Change View: We would downgrade to Sell if Gross Margins fall below 68% (loss of pricing power) or if Order Intake drops sequentially for two consecutive quarters, indicating the Q4 recovery was a false dawn.