The 2026 Artificial Intelligence Industrialization

Financial Architectures, Infrastructure Escalation, and the Transformation of Global Enterprise Value

The fiscal year 2026 marks a decisive pivot in the history of the digital economy, characterized by the transition from generative experimentation to what industrial economists describe as the “AI Build-out.” This period is defined by a colossal redirection of global capital, where the world’s largest technology conglomerates—the “Magnificent Seven” and their hyperscale peers—have committed to a capital expenditure program that exceeds the gross domestic product of several G20 nations. As artificial intelligence evolves from a conversational utility into an autonomous agentic framework, the financial structures of the providers, the cost of the underlying infrastructure, and the valuation models used by capital markets are undergoing a fundamental re-rating.

The underlying data suggests that the global economy is currently navigating a “trough of disillusionment” regarding immediate consumer-facing returns, yet the industrial reality is one of relentless acceleration. Total capital investment in AI infrastructure is projected to reach $700-$800 billion in 2026 alone among the top five hyperscalers, representing a 67% increase over 2025 levels. This investment is not merely a response to speculative demand; it is a forced march toward the creation of a new layer of the global utility grid—the intelligence layer.

The Hyperscale Financial Architecture: Revenue Reacceleration vs. Capital Overhang

The financial narrative of 2026 is dominated by a stark contrast: accelerating revenue growth in cloud services and a concomitant explosion in capital requirements. For the “Magnificent Seven,” the primary challenge is no longer proving that AI can generate revenue, but rather scaling capacity fast enough to capture committed demand while managing the margin compression inherent in massive infrastructure builds.

Revenue Dynamics and the Cloud Reacceleration

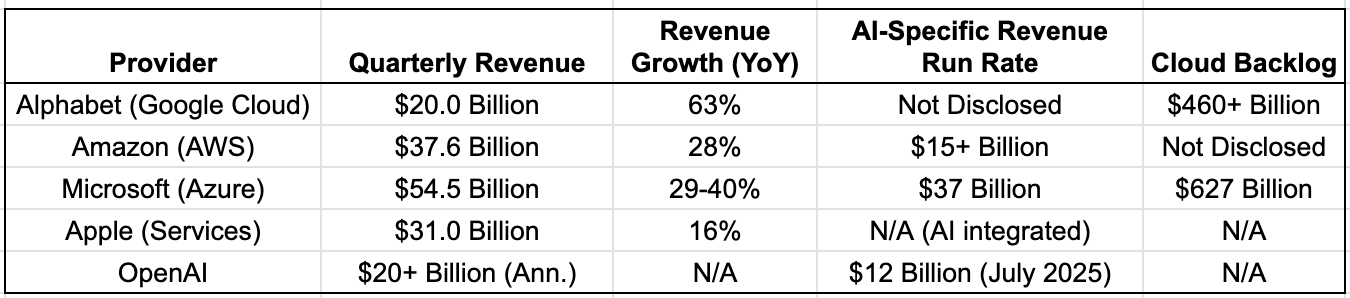

Cloud computing, which many analysts considered a maturing sector in the early 2020s, has seen a dramatic reacceleration. Alphabet, Amazon, and Microsoft have all reported growth rates that defy the traditional law of large numbers. Alphabet’s Google Cloud, for example, reached a milestone in Q1 2026 with a 63% year-over-year revenue increase, exceeding $20 billion for the quarter. This growth is largely attributed to the Gemini family of models and the rapid adoption of Gemini Enterprise, which saw a 40% quarter-over-quarter increase in paid monthly active users.

Amazon Web Services (AWS) has also demonstrated significant momentum, with its AI revenue run rate surpassing $15 billion in the first quarter of 2026. CEO Andy Jassy noted that this growth trajectory is 260 times larger than the original AWS rollout at a comparable stage. Microsoft, meanwhile, has hit an annualized AI revenue figure of $37 billion (+123% YoY), driven by the deep integration of Copilot across its productivity suite and the expansion of Azure capacity.

The Boring Finance Guy 90% May offer is ending soon. Grab your spot at 90% discount for life - and help support TBFG to continue to deliver analysis.

Comparative Financial Performance of Major Providers (Q1 2026)

The analysis of these revenue figures indicates that the market is bifurcating between providers who can offer integrated AI “agents” and those who remain stuck in the “assistant” model. Apple’s performance stands out due to its lower capital intensity. While its peers spend hundreds of billions, Apple’s fiscal second-quarter services revenue of $31 billion grew at 16%, with a gross margin of approximately 77%. This suggests that Apple is successfully leveraging the AI boom through consumer-facing services without the immediate need for the gargantuan data center investments required by pure-play cloud hyperscalers.

The Capital Expenditure Arms Race

If the revenue side of the ledger is promising, the cost side is historic. The five largest spenders—Amazon, Alphabet, Microsoft, Meta, and Oracle—have collectively raised their 2026 CapEx forecasts to roughly $700-800 billion. This spending is heavily weighted toward short-lived assets, primarily GPUs and custom AI accelerators like Amazon’s Trainium and Alphabet’s TPUs.

Microsoft’s CapEx guidance of $190 billion for calendar year 2026 represents a 61% increase year-over-year. This level of spending has created a “CapEx overhang” on the stock price, as investors weigh the long-term benefits of Azure capacity against the immediate pressure on free cash flow. Alphabet’s guidance of $180-$190 billion and Amazon’s $200 billion commitment further illustrate the scale of the commitment.

The primary driver for this spending is the shift toward “agentic” workloads, which are far more compute-intensive than traditional search or generative tasks. A single autonomous agent can consume up to 700 million tokens per week if left running continuously, creating a perpetual demand for inference capacity that existing data centers were never designed to handle.

Infrastructure as a Gating Factor: The Crisis of Power and Compute Density

The 2026 industrial build-out is hitting physical limits. Energy availability, rather than capital or silicon, has emerged as the primary gating factor for AI advancement. The power density requirements for the latest hardware, such as NVIDIA’s Blackwell and the forthcoming Vera Rubin platforms, have forced a radical redesign of the modern data center.

The Global Energy Deficit

Global AI spending is projected to reach $2.5 trillion in 2026, but the physical infrastructure to support this spending is under severe strain. North America is estimated to require 92 gigawatts of additional power capacity over the next five years just to support AI data center demand.

By the end of 2026, the energy consumption of global data centers could reach 1,050 TWh, effectively making the industry the fifth-largest energy consumer in the world if it were a country. This has led to a strategic pivot toward nuclear energy. Meta, for instance, has partnered with nuclear providers like Oklo and TerraPower to secure gigawatt-scale, carbon-free energy for its campuses. Microsoft is reportedly considering shelving its 2030 clean energy targets to prioritize the immediate expansion of its AI capacity, a move that highlights the tension between environmental goals and technological leadership.

Data Center Projections and Operating Metrics (2026)

The scarcity of capacity has driven European data center vacancy rates to record lows of 6.5%. This scarcity is fueling upward pressure on pricing for colocation and wholesale tenants. Companies are increasingly turning to on-site power generation and innovative cooling solutions—such as waterless closed-loop systems—to bypass the years-long wait times for traditional grid connections.

Norway: The Emerging Epicenter of Sustainable AI Infrastructure

Norway has positioned itself as a critical beneficiary of the 2026 infrastructure boom. The nation’s combination of 100% renewable hydropower, a naturally cool climate that lowers Power Usage Effectiveness (PUE), and strong political stability has attracted multi-billion dollar investments from every major AI provider.

The “Gigafactory” of Intelligence: Stargate Norway

One of the most significant projects of the decade is “Stargate Norway,” a $10 billion joint venture between Aker, NScale, and OpenAI. Located in Narvik, this facility is designed as a large-scale AI “gigafactory,” with the capacity to host over 100,000 NVIDIA GPUs by the end of 2026. The project will initially deliver 230 MW of capacity, with plans to expand by an additional 290 MW, making it one of the largest AI infrastructure investments in Europe.

Other major projects include:

Google Skien: An 840 MW data center campus representing a EUR 600 million investment, specifically optimized for proprietary AI frameworks and large-scale cloud storage.

TikTok NO1: A 90 MW facility near Oslo, which Green Mountain plans to expand to 150 MW. At full capacity, this site alone will consume nearly 1% of Norway’s total electricity production.

Bulk Infrastructure N01: Collaborating with national grid companies to add 300 MW of power capacity in 2026 to support high-density compute.

Norway Data Center Construction Market (2025-2031)

The rapid industrialization of the Norwegian energy grid has not been without controversy. Plans to electrify a 350-MW gas facility near Hammerfest, alongside the massive requirements of the AI sector, have sparked public debate over energy prices. The government has intervened with a NOK 60 billion risk relief program and a fixed-price electricity scheme to protect households through 2026.

The Boring Finance Guy 90% May offer is ending soon. Grab your spot at 90% discount for life - and help support TBFG to continue to deliver analysis.

The Competitive Frontier: The Survival Economics of Specialized AI Labs

The 2026 fiscal environment has exposed the stark difference in the economics of foundation model providers versus infrastructure owners. While the hyperscalers leverage cloud revenue to fund AI, pure-play labs like OpenAI are facing a “Code Red” regarding their burn rates.

OpenAI’s $14 Billion Deficit

Internal documents from OpenAI reveal a projected loss of $14 billion for the 2026 fiscal year—roughly triple the company’s 2025 losses. The company is pursuing a $100 billion funding round at an $850 billion valuation to bridge the gap until its projected profitability in the 2030s.

The competitive landscape for OpenAI is deteriorating:

Market Share Erosion: ChatGPT’s web traffic share dropped from 86.7% in January 2025 to 64.5% by January 2026, with Google Gemini capturing much of the loss.

Enterprise Shift: Anthropic has overtaken OpenAI in the enterprise market, holding a 40% share compared to OpenAI’s 27% by H1 2026.

Talent War: OpenAI is facing a significant talent drain, with staff eight times more likely to leave for Anthropic than the reverse. The company expects to spend $6 billion on stock-based compensation in 2026 just to retain key engineering talent.

Anthropic and Perplexity: The Rise of Specialized Competitors

Anthropic has emerged as the primary beneficiary of enterprise caution, growing its revenue from $1 billion ARR in 2024 to more than $9 billion by late 2025, with projections of $40-50 billion for 2026. Meanwhile, Perplexity has disrupted the search market by launching its “Computer” agent, coordinating 19 different models (including Claude, Gemini, and GPT-5.2) behind a single interface. Perplexity’s shift away from advertising toward a “Perplexity Max” $200/month subscription and usage-based credits reflects a broader trend of monetizing high-value autonomous work over simple information retrieval.

Capital Markets and Stock Valuation: Navigating the CapEx Overhang

The 2026 stock market for AI providers is characterized by extreme volatility and a “show me the money” attitude from institutional investors. While fundamentals remain robust, valuation multiples are being compressed by the sheer scale of the required investments.

Microsoft (MSFT): The Market’s Cautionary Tale

Microsoft enters its fiscal Q3 2026 in a unique position. Despite reporting revenue growth of 18.3% and beating EPS estimates, the stock is down 14% year-to-date as of May 1, 2026.

The primary factors weighing on MSFT include:

CapEx vs. FCF: Investors are focused on the $190 billion CapEx guidance, which is tracking toward $104 billion for the current fiscal year alone, squeezing near-term free cash flow.

OpenAI Partnership Changes: A revised agreement announced in April 2026 ended Microsoft’s exclusivity over OpenAI models and capped revenue-share payments through 2030, introducing uncertainty about the long-term ROI of the partnership.

Technical Resistance: MSFT is currently trading near $418 (-13% YTD), caught between its 100-day and 200-day simple moving averages. Analysts maintain a “Buy to Stong Buy” consensus with an average target of $570, but many have trimmed their targets to account for the CapEx overhang.

Alphabet and Amazon: The Cloud Resilience Case

In contrast, Alphabet (up 23.1% YTD) and Amazon (up 16.4% YTD) have been rewarded for their cloud acceleration. Alphabet’s 63% cloud growth was significantly stronger than Microsoft’s or Amazon’s, and its ability to power its AI through custom TPUs provides a clearer path to margin expansion.

Amazon’s $200 billion CapEx is viewed more favorably because it is tied to specific, unannounced customer commitments and a $20 billion run rate for its custom AI chips.

Analyst Sentiment and Technical Indicators (May 2026)

The Long-Range Horizon: 2030 and the Jagged Frontier

As the world moves toward 2030, the economic impact of AI is expected to transition from infrastructure spending to broad productivity gains.

GDP and Productivity Projections

Morgan Stanley and Goldman Sachs estimate that $4 trillion to $8 trillion will be invested in AI CapEx over the next five years. This investment is expected to contribute approximately 2.5% to U.S. GDP growth in 2026 and more than 3% by 2027.

By 2035, AI is estimated to have a permanent effect on the level of economic activity:

GDP Level Increase: 1.5% by 2035, growing to 3.7% by 2075.

Labor Cost Savings: An average of 25% across exposed sectors, potentially reaching 40% as adoption saturates.

Sector Exposure: Approximately 40% of current labor income is potentially exposed to automation by generative AI, with the strongest impact in the early 2030s.

The “Jagged Frontier” of Capability

Technical performance in 2026 continues to follow what researchers call the “jagged frontier.” Models can now solve PhD-level science questions and meet near-100% human baselines on coding benchmarks like SWE-bench. However, basic physical reasoning remains flawed; for example, the top-performing models still fail to read analog clocks correctly nearly 50% of the time.

This dichotomy suggests that the “Future of AI” is not a linear progression toward general intelligence, but a specialized evolution of “agentic” capabilities. The companies that will thrive in this environment are not necessarily those with the largest models, but those with the most efficient infrastructure, the most secure orchestration protocols like MCP, and the most flexible monetization models that can capture the value of autonomous work.

The 2026 industrialization is the most significant capital event in the history of technology. While the costs are astronomical and the energy requirements are straining the limits of the physical world, the emergence of a trillion-dollar intelligence economy is no longer a matter of speculation. It is a matter of installation. In this new era, the distinction between a “software company” and a “utility provider” has effectively vanished, as intelligence becomes the primary resource of the 21st century.